Table of Contents

The experienced long-term disability lawyers at Bross & Frankel have represented thousands of clients in more than twenty years of practice. We advocate for people who have individual disability policies, as well as those with group disability policies offered through their employers.

The long-term disability insurance attorneys at Bross & Frankel can help you receive your full long-term disability benefits by providing a wide range of services, including:

- Long-Term Disability Claim Review

- Application Assistance

- Appeals for Denied/Terminated Private Insurance LTD Benefits

- Appeals for Denied/Terminated ERISA Benefits

What Is Long-Term Disability Insurance?

Long-term disability (LTD) insurance is a specialized type of insurance policy that protects you in the event that you are unable to work due to a disability. While workers’ compensation benefits will typically protect you if you are hurt or become ill on the job, a long-term disability policy offers you benefits if you suffer from an illness or injury that is unrelated to work. In other words, it is income protection insurance.

LTD insurance can often be purchased through your employer’s group plan or may be purchased individually. In most (but not all) cases, if you have coverage through a group plan, then the policy is governed by a federal law known as the Employee Retirement Income Security Act of 1974, or ERISA. This law sets out specific standards that must be followed, including requiring insurance companies to provide certain information to policyholders and to set up an appeals process.

Under ERISA, policyholders can file a lawsuit in federal court for wrongful denial of a claim or another reason, such as improper termination of benefits. Policies that are not subject by ERISA are governed by state law. If a lawsuit is filed regarding these LTD policies, it will be heard in state court.

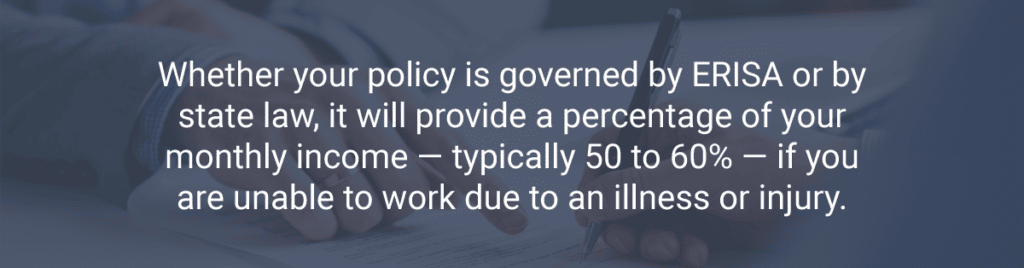

Whether your policy is governed by ERISA or by state law, it will provide a percentage of your monthly income — typically 50 to 60% — if you are unable to work due to an illness or injury. In addition, many policies will offer rehabilitation services and/or incentives to help you return to work sooner. These benefits are available after a waiting period, which is usually when you have been out of work for 6 months.

Long-term disability insurance is an important part of any overall financial plan. However, many insurance companies make it difficult to be approved for LTD benefits. Bad-faith delays, denials of disability insurance claims, and early termination of coverage are all-too-common.

Hiring an experienced long-term disability attorney early in the process can help you obtain the highest possible level of disability benefits. A long term disability insurance lawyer can examine your LTD policy and explain its terms, conditions, and limitations, enabling you to make a strategic decision about how and when to apply for benefits. With an advocate to guide you through the process, you are less likely to have the process delayed — or to have your claim denied outright.

How Insurance Companies Deny Valid Disability Insurance Claims in New Jersey

If you have a long-term disability policy, you may think that you will automatically receive benefits if you can’t work due to a disability. But just like other types of insurance, it often isn’t that simple. Long-term disability insurance companies look for reasons to deny or delay claims because their main business isn’t to pay out on claims — but to make money.

Insurers use a variety of reasons to deny legitimate long term disability claims. An insurance company may deny your application on the basis that you have not proven that you are disabled, even if you have submitted mountains of medical records to back up your claim. Alternatively, the insurer may use its own independent medical professional’s opinion to make a determination that you are not truly disabled, or that you are still able to work.

In some cases, an insurance company may argue that you have a pre-existing condition that is excluded from coverage. A skilled long-term disability lawyer can cut through the legalese and demonstrate that your condition isn’t subject to an exclusion. Depending on the type of policy that you have, this may mean following a strict appeals process before ultimately filing a lawsuit in federal court.

There are other ways that insurance carriers may deny your legitimate long-term disability claim. Many ERISA plans also have two different definitions of disability you may have to meet in order to continue receiving LTD benefits. Doing so can be complicated — particularly if you are unfamiliar with the system and the process.

When you work with a seasoned disability benefits attorney from the start of your case, it puts you at a distinct advantage. Many denials are based on specific policy terms. Having a lawyer examine your LTD policy and base your application on the terms and conditions of your policy can help to avoid any delays — and possible denial of benefits.

One of our clients experienced how smoothly the process can be when you work with a long term disability lawyer from the start:

Excellent legal help! Did amazing work on my disability case. Compared to the normal wait, I was approved extremely quick and did not need to testify in front of a judge (something I was terrified of). Highly recommend their services!

While each case is unique and results are not guaranteed, having an attorney to advocate for you can help you achieve a better outcome.

How Can You Appeal Denied Long Term Disability Benefits?

If your application for LTD benefits is denied, the next step will depend on the type of policy that you have. Because the law governing disability insurance policies is complex, it is important to consult with a long term disability benefits attorney as soon as possible if you receive a denial letter.

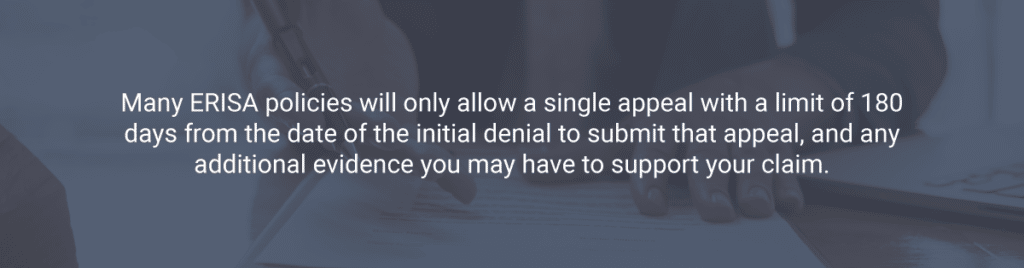

ERISA benefits have strict deadlines that, when missed, can seriously limit or forever prevent a disabled worker from getting disability benefits. Many ERISA policies will only allow a single appeal with a limit of 180 days from the date of the initial denial to submit that appeal, and any additional evidence you may have to support your claim. If the LTD insurer again denies the claim, your only remaining recourse would be to file a federal lawsuit to try to obtain your benefits.

Bross & Frankel’s ERISA long term disability attorneys have the experience and knowledge necessary to address the insurer’s reasons for denying your claim. We’ll get to work to give your appeal the best chance of success.

If you have been denied long term-disability or your benefits have been terminated, or if you have questions about how to apply for benefits, contact our attorneys today.

Contact Us Today

To schedule a free LTD claim review or to learn more about how we can help you, contact our office today at 856-795-8880.

Schedule A Free LTD Claim Review

What is ERISA And How Does it Affect My Disability Claim?

What would you do if an illness or injury left you disabled and unable to work for days, months, or ever again? Every year, thousands of people become disabled before they reach the age of retirement. Long term disability insurance offers benefits, usually based on a percentage of your salary, during the time you are unable to work. Many employees are aware that they receive health and retirement benefits through their employer, but fewer know if they have long term disability coverage, or what type of disability coverage they have.

When you need to draw on your disability coverage, it can make a difference if your policy is governed by the federal Employee Retirement Income Security Act, better known as “ERISA.” This is because ERISA, unlike an insurance policy you might purchase yourself from an insurance agent, provides legal protections to employees, as further discussed in this article. Most group disability plans provided by your employer are governed by ERISA. But private policies you purchased on your own are not.

What Exactly is ERISA?

The Employee Retirement Income Security Act of 1974 (ERISA) was enacted to set minimum standards for employee group benefits including health, life, and disability benefits. ERISA protects benefit plans from mishandling and abuse, and ensures that employers are acting in the best interest of their employees. ERISA regulates how disability plans are managed by the employer including how disability claims are to be processed, deadlines for filing a claim, and an employee’s rights if their long term disability claims are denied.

ERISA also requires accountability and transparency, to guarantee that employees have access to information about their benefit plans. Any employee covered by their employer’s disability benefit plan should receive a written summary of their plan detailing key features: how the disability plan works, what benefits are offered, and any out-of-pocket costs to be incurred by the employee for coverage.

When Does ERISA Apply?

An individual may choose to purchase disability insurance on their own or it can be provided by an employer. Some states require employers to provide disability benefits for their employees, including New York, New Jersey, California, Hawaii, and Rhode Island. Employers operating in these states must provide disability insurance regardless of where the employer’s corporate offices are located. Employers who do not provide disability coverage in these states may be subjected to fines and penalties. Who provides the insurance may determine whether the disabled individual is covered by ERISA.

The protective laws of ERISA only apply to private-sector companies that offer employer-sponsored benefits. It is irrelevant whether the private company is organized as a partnership, corporation, LLC, or a non-profit. Although ERISA provides protection to people who work for most types of employers, ERISA does not ordinarily apply to:

- Privately purchased, individual insurance policies or benefits

- Benefit plans offered through state, local, or federal government employers

- Benefit plans offered through church employers

- Benefit plans that are maintained only for purposes of complying with workers’ compensation, disability, or unemployment laws

- Unfunded excess benefit plans

- Plans that are maintained outside of the United States and are intended primarily to benefit non-resident aliens

If you don’t know whether your disability coverage is governed by ERISA, you can start by asking the human resources department at your place of employment. However, if your disability claim has already been denied or terminated, it may be time to speak to a ERISA disability attorney to help you advocate for your rights under your policy and ERISA.

Why Is Hiring An ERISA Long Term Disability Attorney Important?

When an injured individual files a disability claim, their insurance company or employer may attempt to deny the employee’s claim. The claim may be denied because the employer alleges that the individual is not disabled, they are not covered by the policy, or that the employee failed to follow the proper guidelines when applying for benefits. It is important to understand whether ERISA governs the long term disability insurance claim because ERISA provides the right to appeal a claim denial and file a lawsuit to compel coverage.

How Does ERISA Affect My Long Term Disability Claim?

When an employee is covered by an ERISA-governed plan, the federal law provides a number of protections to help the employee obtain disability benefits. If an employee’s disability benefits are denied, ERISA demands the claimant receive copies of any documents, records, or information relevant to their claim for benefits, free of charge on request. Following an adverse decision, ERISA also requires that the claimant be allowed a full and fair review through an appeals process.

While ERISA provides certain protections for employees, ERISA has been interpreted in a way that also significantly benefits insurance companies near you. Perhaps most importantly, if the denial of your claim is upheld on appeal, in most cases, you cannot add additional evidence to prove your disability. In addition, if you have to go to court, a judge may be required to review the denial under an “arbitrary and capricious” standard of review. That means, even if the judge would have found you disabled, he or she can only overturn the insurance company’s decision if it is without a rational basis. Simply put, proving the insurance company’s denial was wrong may not be enough.

There are numerous ways in which ERISA effects disability claims, but the bottom line remains this: the primary purpose of ERISA is to safeguard employees who are counting on benefits that their employer promised them. ERISA is a broad and complex federal statute, and the protections that it affords claimants stated above are by no means exhaustive, and as noted above, ERISA may also negatively impact your rights, making it vitally important that you obtain all the evidence you could possibly need to prove your claim before the insurance company makes a “final” decision. For that reason, it is imperative to consult with an experienced ERISA attorney to explain your rights and fight for the benefits that you deserve.

We Take on Insurance Companies of All Sizes

Our long-term disability lawyers have helped New Jersey residents with their claims and appeals of denied benefits from insurance companies both large and small. We have advocated for clients with a range of insurance plans and insurance companies, including:

- The Hartford

- CIGNA

- Liberty Mutual

- Prudential

- MetLife

- Aetna

- Unum

- Sun Life

- Lincoln Financial

- MassMutual

- Dozens of other private and ERISA disability insurance companies

Having an ERISA attorney who is familiar with long-term disability claims and the private disability insurance companies that deny them is vital to the success of your case. This is a difficult and specialized area of the law. Our firm only takes cases that we think we can win, and in most cases, we only earn a fee if we do.

When talking to an ERISA long term disability attorney — even if it isn’t us — make sure that you feel comfortable that he or she knows how to fight LTD denials and win. Any lawyer that you talk to should also be realistic about the difficult hurdles the insurance companies and the law have put in front of people. The attorney-client relationship is an important one and should be built on trust, starting with honesty about the process.

Nobody wants to have to use long term disability insurance, but you want it to be there for you when you need it. When a claim is denied or terminated, that’s why we get to work when you can’t ®️.Contact us or call us today at 856-795-8880 for a free consultation and case evaluation.

Related: